Imagine being able to take the pulse of hundreds of petfood industry experts from around the globe, honing in on every major market and region with all its diversity, complexity and interconnections. Through an online questionnaire distributed by Petfood Industry during December 2006 and January 2007, Packaged Facts/Petfood Industry's Global Survey did just that, compiling the responses of nearly 500 readers of the magazine, including manufacturers, suppliers, service/consulting firms, marketers, veterinarians and nutritionists, to gauge future trends in the global petfood industry as well as the current state of industry development in individual national markets. Highlights include:

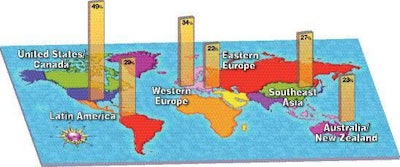

A total of 59 countries are represented in the survey, and a majority of respondents' companies do business in multiple regions, with the largest percentage citing involvement in the United States/Canada (74%), followed by Western Europe (61%), Southeast Asia (61%) and Latin America (57%). In addition, significant proportions are associated with petfood markets in Australia/New Zealand (48%), Eastern Europe (47%), North Africa/Middle East (39%), India/Pakistan (33%) and South/Central Africa (30%).

Most respondents work in general management (29%), marketing/sales (28%) or research (14%). In terms of their locations, half of respondents work with the US/Canadian markets and a third with Western Europe, while one-fifth to one-quarter work with markets in each of the other regions (see Figure 2). In keeping with this multiregional emphasis, the regional data reflect broad market perspectives rather than local market performance.

The dozens of global market trends covered in the survey are grouped under 12 broad factor headings: new product trends, cultural shifts, product pricing, branding, globalization, packaging trends, marketing and trade, demographic trends, retail and supply shifts, marketer shifts, Internet use and organic petfood.

The survey results, detailed in Packaged Facts' May 2007 Global Pet Food Industry Outlook report, further classify national markets into three levels of development, mature, mid-level and emerging, based on respondents' characterizations of pet ownership rates, degree of pet pampering/humanization, level of health/veterinary care and prevalence of mass market and premium petfood brands in their countries of residence (see Figure 1).

To put the survey data in context, the report also draws on primary interviews with industry executives and professionals; syndicated pet market reports published by Packaged Facts; government, trade and consumer research sources; and Datamonitor's Productscan Online service tracking new product introductions worldwide.

Top global factor: new product trends

Of the 12 broad factors covered in the survey, new product trends is number one overall, with two-thirds (66.7%) of respondents considering it very important to the development of the global petfood industry during the next five years (see Figure 3). The most important components of this factor are:

Functional/condition-specific/novel ingredient foods (lifestage, weight loss, breed-specific, therapeutic);

High-growth segments such as treats;

Hyperpremium products; and

Human-grade ingredients.

New product trends places high on the list of all respondents, regardless of company type or professional role. More than three-quarters (75.8%) of petfood manufacturers cite this factor as very important, making it the top-ranked among this group. For retailers, the factor tops out at 85%. Among all respondent roles, new product trends ranks first except for veterinarians and respondents holding university/researcher/scientist positions.

Considering the nine regions in the survey, new product trends heads the list for five and holds second place for all but one of the othersSouth/Central Africa, where it is third. Tellingly, this factor rates even higher in the less developed markets of South Asia (77.4%) and North Africa/Middle East (74.2%) than it does in the developed markets of North America (71.6%) and Western Europe (69.7%), signaling the strong interest in commercially prepared petfood in emerging markets.

Cultural shifts is the other global factor cited as very important by more than 60% of respondents. The most important facets of this factor are the human/pet relationship and ability of consumers to afford pet care. Of the remaining 10 factors, seven are judged to be very important by 54%-60% of respondents, while three fall below this level. Organic petfood comes in last at 31%, reflecting both the low penetration of organic products in mature markets as well as the much lower level of interest in mid-level and emerging markets.

Human/pet relationship heads trend list

While new product trends scores highest among the 12 broad factors, three individual elements (specific aspects comprising the broad factors) rate even higher. The human/pet relationship, an aspect of the cultural shifts factor, rates as very important among almost four-fifths (78%) of survey respondents.

Convenience, under the packaging trends factor, and special ingredient foods (i.e., functional/condition-specific/novel ingredient foods), under new product trends, each garner "very important" votes from 68%. The three elements placing lowest in the survey, each ranked very important by less than 25% of overall respondents, are homogenization of product preferences (under globalization), postponing marriage (under demographic) and global production (under organic petfood).

South Asia: high priority on marketer shifts

Looking across all four respondent classifications, company type, professional role, level of country development and region, an even 78% of marketers cite branding as being very important to the petfood industry during the next five years, making this the highest-ranking trend by this measure. More than three-quarters of two other classifications, respondents from South Asia and manufacturers, say new product trends is very important, at 77% and 76%, respectively.

By index, the highest ranking factor is marketer shifts, as rated by respondents who work in or with regions including South Asia. These survey participants are 36% more likely than all respondents on average (index of 136) to view this factor as very important. As in other emerging markets, the petfood fortunes of South Asia (i.e., India and Pakistan) depend on the advances of Western influences into the market, via manufacturers like Mars division Effem India Pvt. Ltd. (Pedigree) and international retailers like Wal-Mart and Carrefour.

New products expanding to less developed markets

Last year saw the biggest global surge of new petfood products ever, with a growing share of the activity coming from mid-level and emerging markets in Eastern Europe and Latin America (see Figure 7, p. 25). During 2006, 655 new dog and cat food products appeared globally, up from 280 in 2002, according to Datamonitor's Productscan Online service.

In the US, which accounted for approximately half of 2006 introductions in mature country markets, marketers launched 254 new dog and cat food product lines encompassing 1,181 SKUs (including different flavors, sizes and package variations), up from 155 lines and 587 SKUs in 2002.

Premium petfoods cover all bases, natural/organic, fresh/real, fortified/functional, breed/size specific, and are increasingly being positioned not just as human style but also human grade in terms of ingredients and manufacturing processes. This trend seems likely to gain further steam given the recent petfood recalls in the US and Canada.

Trends trickling over

Despite the vast differences in the three levels of market development, the global petfood market may be smaller than one might expect in terms of the trends expected to drive growth through 2011. The human/pet relationship trend topping the list in mature markets also ranks high in mid-level and emerging markets, with at least 70% of respondents for each level of development citing it as very important.

In mature markets like the UK and Australia, the humanization trend will continue to involve products that more closely resemble those for people, while the most important aspect of the human/pet relationship in emerging markets like China and Russia will be increased levels of pet ownership and commercial foods penetration. In mid-level markets, this trend will track between those two scenarios.

As major marketers continue to expand their international presence, expect to see a rapid acceleration in global overlap of trends like functional foods, urban-centric marketing and Internet marketing as mature market trends trickle over into less developed markets.