The cat and dog petfood market has seen dynamic shifts from major players in recent times. Mars, Inc. recently acquired Doane Pet Care, the largest maker of private label dog and cat food in the US and Europe. This merger was a significant development and requires further insight on how it affects the petfood marketplace.

Mars, which holds the lion's share of the petfood market (approximately 25%, before the Doane acquisition), decided to strategically focus on the private label segment. Though this acquisition was expected to provide production capacity and accelerate the innovation pipeline (which would strengthen and grow their pet business in North America), the implications of this move could impact the balance of power within the private label arena, targeting major players in the US, as well as players in international markets.

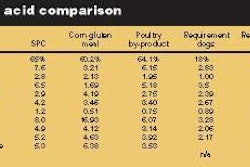

The US private label petfood market

Doane Pet Care is the largest manufacturer of private label petfoods and the second-largest producer of dry petfoods in the US market. Doane not only supplies some national brands, and approximately 175 store brands, but also supplies product to support the Ol' Roy brand of dog food and Special Kitty brands for the mass merchandiser Wal-Mart.

In 2003, dry dog food accounted for 46% of the market share of all private label petfood product. Sales were skewed higher by Wal-Mart private label dog food brands. In 2006, this trend continues with Wal-Mart seeing a +3% growth rate versus last year of its US$3.4 billion petfood business.

Strong year-over-year performances in Wal-Mart's private label sales have fueled the Doane Pet Care bottom line. Wal-Mart is Doane's largest customer, representing about 65% of Doane's business. It is evident that this strong financial contribution, coupled with the leverage Mars now has in negotiating power with the most powerful retailer in the world, is a brilliant strategy for maintaining market dominance in the petfood segment.

The international petfood market

The acquisition of Doane Pet Care also gives Mars a competitive advantage internationally. Globally, private label petfoods account for approximately 21% of all private label commodities sold, and is projected to grow at 11% per annum with private label dog food (12%) more than doubling the growth of manufacturer brands (5%). Most of the growth comes from countries such as New Zealand, Portugal, Puerto Rico, Mexico, Finland, Sweden, Brazil and Argentina. Mars, Inc. has the capacity and global experience to strategically play in these international markets and is well positioned to do so given the growing demand internationally for private label petfoods.

While growing up in Jamaica, and being the proud owner of 12 dogs at the age of 13, we fed our dogs the typical canine cuisine of "turn," or corn meal flavored with last night's leftovers. So, going to the local supermarket or store to purchase dog food (either a manufacturer or store brand) was not a routine concept. In less developed countries awareness is shifting as brand awareness and low prices allow for easier market penetration. I suspect that Mars may have seen this as a significant opportunity and has made a very innovative move to become a greater part of this global growth market in private label petfoods.