The petfood industry has exhibited little fluctuation in the level of imports and exports throughout the recession, especially when compared to swings in the overall trade market. Pet owners and manufacturers realize the necessity of such products, and therefore the industry continues with little volatility. January and February started 2011 off strong with increases in both vessel imports and exports. Imports are up 29% this year compared to last year and exports are up nearly 7% (Figure 1, see "More Images" tab at top).

The largest supplier of cat and dog food to the US for vessel imports is China, posting an impressive 70% import market share in the industry for February. Other top suppliers include Thailand, with an import market share of 25% (Figure 2).

While Cambodia’s current import market share is only 2%, that country recorded a noteworthy rise in exports to the US: a 114% increase from February 2010 to February of this year. Costa Rica also showed a very healthy year-over-year increase of 260%.

Japan is the largest buyer of pet food from the US; 50% of all US vessel exports of dog and cat food are destined for that country (Figure 3). Other top destinations include Australia and Taiwan, though the latter saw declines in both value and weight from February 2010 to February 2011.

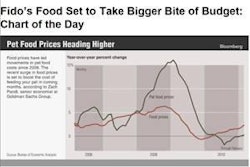

Pricing analysis of vessel imports shows a 14% increase in the cost per kilogram from February 2010 to this February, increasing from US$3.68 per kilogram to US$4.19 per kilogram. Vessel exports saw a 16% rise in the cost of exports, increasing from US$1.61 per kilogram to US$1.87 per kilogram.

Similarly, the outlook for pet food imports and exports continues to be positive. The global demand for pet food is not likely to decrease drastically, even through price hikes, because of the necessity of such products. Recent fuel spikes will likely push prices even higher in the near future and shifts in suppliers may occur; however, the market will probably not experience a large slowdown.