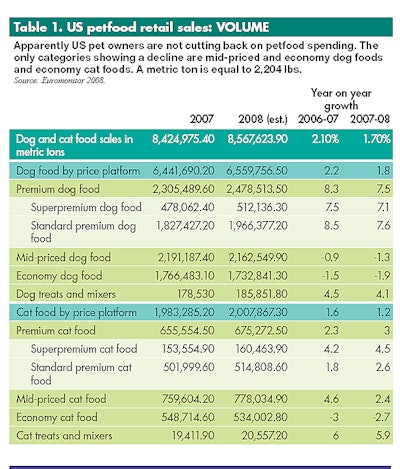

Apparently US pet owners are not cutting back much on petfood spending. The only categories showing a drop in volume are mid-priced and economy dog foods and economy cat foods. Given the troubled economy and gas prices, it doesn't seem logical. Maybe because petfood buying is becoming more and more emotional - combined with US pet owners focusing more on quality, taste and function rather than price.

Profitability down

A sharp increase in raw material costs is hurting the short-term profitability of petfood manufacturers. However, the longer-term trend toward premiumization has not been undermined, at least in developed markets.

Although manufacturers are raising unit prices, the unavoidable lag between costs rising and those costs being passed on to consumers will inevitably undermine short-term margins. This lag has been lengthened by the unexpected severity of recent increases. In the first quarter of 2008, rising raw material costs increased Colgate-Palmolive's cost base (across its entire operations) by 3% to 4% more than the company had anticipated. As a result, in an April 2008 conference call on its results for the first quarter of 2008, the company predicted that its full-year gross profit margin would be flat.

Similarly, Meow Mix and Kibbles n' Bits manufacturer Del Monte is now predicting earnings per share for continuing operations in the range of US$0.64-0.68 for the full fiscal year, below the consensus expectation of US$0.77. It would be reasonable to anticipate that other petfood manufacturers will be similarly impacted, resulting in a softening of margins during the first half of 2008, before they recover later in the year.

Value still outpacing volume

Some market researchers believe there is less price elasticity in the demand for petfoods than for human food, and the industry's latest sales figures are bearing this out. Like their counterparts in packaged food, petfood manufacturers are weathering a surge in raw material costs. With cereal prices rising sharply on commodity markets (wheat hit a record high on the Chicago Board of Trade in February, soaring above US$10 a bushel), the cost of such petfood staples as corn gluten meal, brewer's rice and wheat gluten are being pulled upward, and manufacturers must also cope with increasing energy and transportation costs. While it would appear that, on the whole, manufacturers are successfully passing on much of these increases to consumers, their short-term profitability is undoubtedly being affected.

According to Euromonitor International data, global petfood sales are likely to post value growth of 6.1% in 2008 to reach US$52.8 billion, but volume growth of only 2.2%. While this indicates that the premiumization of the petfood market is continuing quickly, these figures do not represent a significant break with the medium-term trend - value growth has outpaced volume growth in petfood by more than 2:1 for most of the current decade - and significant unit price increases have been introduced during recent months.

Price increase options

According to Michael Sapp, VP of dog and cat consumables at the US chain PetSmart, the cost of Hill's Science Diet dog food has risen by about US$2 a bag to around US$36 during the opening months of 2008. Some of its rivals have taken a more indirect approach by shrinking package sizes and leaving prices unaltered. Large bags of Purina Dog Chow have been reduced in size from 50 lbs. to 44 lbs. (or 22.5 kg to just under 20 kg), but the retail price at PetSmart has remained the same, at around US$17. Similarly, Mars has reduced the size of its large Pedigree Complete Nutrition from 44 lbs. to 40 lbs. (or 20 kg to 18 kg), but its PetSmart price is unaltered at around US$18.

In Asia-Pacific, the Hong Kong market has seen even stronger price increases. Speaking in April, Tweety Tam, merchandising manager at the local chain Pet Central, said that a 2 kg package of dog food had risen by HK $25 (US$3.20) to HK$170 (US$21.76) during the previous month. According to Tam, some importers are exploiting rising costs "by drastically increasing the wholesale price." With consumers in this region already concerned about rice shortages, this worry could easily spill over into petfood. Indeed, the fact that some products were out of stock for two months suggests at least a degree of panic buying.

Logic + emotion

Consumers appear to be accepting these price increases in spite of declining real disposable income and falling consumer confidence. They are refusing to either trade down to cheaper brands or shift from more expensive wet to cheaper dry products. Due to deepening anthropomorphism, pet owners are becoming even more brand loyal. Many owners hold the view that their pets can tell the difference between different products and they are therefore reluctant to switch brands in case it upsets their pets' digestive systems. This process may well have been aided by the 2007 recall of tainted petfood, as many pet owners are now even more reluctant to feed cheap products to their animals as they perceive them as being possibly unsafe.

Against this background, the longer-term impact of rising prices (assuming that costs remain elevated) is likely to prove relatively benign, at least in developed markets. The trend toward premium and natural products, including organic and eco-friendly items, is both well established and robust. Moreover, if these cost increases prove to be short-lived (given there is a distinct possibility that recent commodity price rises are influenced by speculative capital), the long-term impact on margins could actually be positive, as recent consumer behavior indicates a willingness to choose petfood products on quality, taste and function rather than price.

Slowdown in developing markets

However, in developing markets, the longer-term impact of rising prices is likely to be more significant as it will inevitably retard the industry's maturation by slowing the substitution of packaged petfood for table scraps at the lower end of the market. As a result, Euromonitor International data shows that annual value growth of dog and cat food sales in China slowed from 8.5% in 2006 to a projected 7.3% in 2008. This may also create new opportunities for indigenous manufacturers (particularly those that source the bulk of their raw materials locally) to gain market share from their higher-cost foreign rivals, at least in the economy segment.

.png?auto=format%2Ccompress&fit=crop&h=167&q=70&w=250)

.png?auto=format%2Ccompress&fit=crop&h=167&q=70&w=250)