The Ukrainian market of ready-to-use petfood for cats and dogs is still in its formative stages. According to Kormotech Petfood Nutrition Company statistics, the number of dogs in Ukraine is 750,000 and the number of cats is about 5.5 million. Ready-to-use petfood market permeability (the number of pet owners who do feed their pets with ready-to-use food) is 30%–35%, while in Europe and the US the figure is over 70%.

Current status

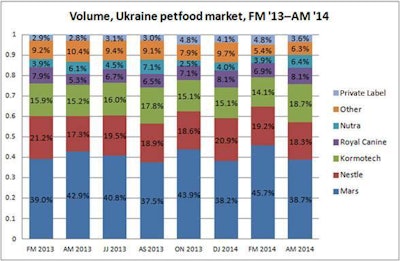

At the end of 2013, the Ukrainian petfood market was worth UAH3.3 billion (US$300–320 million) and produced more than 90,000 tons of dog and cat food. The 2010–2013 growth rate was about 6% in actual measurement and more than 15% in cash per annum. In terms of petfood segments, the economy/standard/premium/superpremium breakdown is weighted in the middle: 2/30/46/22, respectively. As for the types of petfood (dry/cans/pouches), the segments clearly favor canned—47/16/47, respectively.

Currently, the dry petfood market is showing stagnation, partly due to reduced demand for dry dog food. There are also slight declines in the categories of dry cat food and canned cat food because the market has been redistributed towards pouches. At the same time, pouches are showing the most dynamic growth in the cat and dog food market. In the coming years, the growth rate of the pouch market is expected to remain steady at 3%–5%.

Ukraine has multiple channels when it comes to selling petfood, and consumers are taking advantage of all of them. According to the latest data from Ipsos Company, the monthly breakdown of shoppers is:

- Pet stores: 84%

- Supermarkets: 77%

- Grocery stores: 40%

- Breeders: 5%

- Online stores: 3%–5%

Future outlook

The hryvnia (Ukraine's currency) devaluation up to 70% at the beginning of 2014, the situation in the East and the Crimea annexation will continue to adversely affect petfood market dynamics during 2014–2015. According to estimates, in 2014 the market will decrease by approximately 8% in actual measurement and will remain around 2013 numbers in cash.

In 2013 there were 20,000 outlets which sold cat and dog food (3,700 – pet shops, 2,500 – supermarkets, 14,000 – grocery stores and stalls). The range in pet shops is similar to that in supermarkets and grocery stores. In an inflationary environment, supermarkets are trying to keep petfood prices through their leverage and as a result give the consumer a better price, which adversely affects pet shops. The pet trade channel in Ukraine is weak, as there are no large players (networks) and existing pet shops owners do not have the resources for growth and development and, as a result, cannot compete with supermarkets. Therefore, in the next year or two the number of pet stores will reduce.

In 2015–2017 the market will resume growth by approximately 3%–4% in actual measurement and by roughly 7%–10% in cash. In 2014–2015 demand for products made ​​in Ukraine will increase, in particular, because of growing consumer patriotism. During 2014–2016 a growing demand for cat products in the middle price segment is expected, and 2016–2017 will see an increased demand for more expensive products (in line with world trends). Growth of premium and superpremium categories will be directly proportional to income growth. In 2014–2017 the continued growth of pouch segment for cats is anticipated, and by 2017 the market will grow by 7% in volume and by 22% in cash.

Above data are based on studies conducted by AdvanterGroup, ComConUkraine, Ipsos Ukraine, Soyuz-Inform and the Kormotech Company.