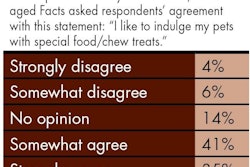

Rising sales plus declining costs add up to a positive direction for any business or industry. Based on news wrapping up 2011, that may be the direction for petfood this year.

Data from Euromonitor International in early December 2011 showed global petfood sales grew 4% last year, keeping pace with the 4.4% increase the entire pet product industry saw from 2009 to 2010. The 2011 rise in petfood sales was fueled by 11.9% growth in Eastern Europe and 9.3% growth in Latin America, followed by 4.6% in Australasia, 3.9% in Asia Pacific and 3.5% in North America. The Middle East and Africa recorded 2.4% growth, while Western Europe barely registered with a 1% increase.

That all added up to US$65.8 billion in sales worldwide, compared to US$63.3 billion in 2010. Note that these data comprise all categories of petfood. When you look at just dog and cat food, the growth rates are nearly the same, with 2011 sales at US$61.8 billion.

With volume, global sales of petfood in metric tons grew just 1.8%, totaling 21.1 million tons as of December 2011. Dog and cat food volume accounted for the bulk of that (20.6 million tons).

Eastern Europe saw 6% volume growth and Latin America had nearly 5% growth. Asia Pacific volume actually declined 3.2% year over year, despite the 3.9% sales gain for that region. With Japan the dominant petfood market there, the natural disasters it suffered likely had an effect, though other countries probably helped pick up the slack in sales. (India, China and Thailand are among the fastest-growing petfood markets worldwide, Euromonitor says.)

So-called developed regions like North America and Western Europe had volume growth just below or above 1%; Australasia hardly grew in volume at all (0.28%). Value sales gains in these regions likely came from premium and superpremium sales and price increases, largely due to rising ingredient costs, which reached record levels in 2011.

Yet also in December, during US Poultry’s Grain Forecast and Economic Outlook Conference, Paul Aho, economist for Poultry Perspective, predicted a bushel of corn would fall to about US$5 over the next two years, compared to US$6.58 a bushel as this issue went to press. His prediction also compared favorably to the US Department of Agriculture’s November 2011 World Agricultural Supply and Demand Estimates, which pegged a farm price of US$6.20-7.20 per bushel of corn for the 2011-12 crop year.

Another expert on the US Poultry panel, Tim Brusnahan, VP of consulting for Brock Associates, said his company projected corn at US$5.75-6.50/bushel for the 2011-12 crop year and US$5.25-6.25/bushel for 2012-2013. He added that the price could fall below US$5/bushel if economic growth is really small and demand for gasoline drops, which will in turn hurt ethanol demand.

Corn and energy prices are closely linked because of biofuel policies in the US and EU. Last year, for the first time ever, more corn went into ethanol production than to feed livestock and poultry in the US; yet January 1, 2012, marked the end of the US federal subsidy for corn ethanol, which amounted to roughly US$6 billion a year. Even if your petfood formulations don’t include corn, its pricing, supply and demand affect those of other grains and commodity ingredients, so an increase in the supply of corn along with a decrease in its price is good news for petfood producers. (Learn more about commodity prices and availability at Petfood Forum 2012; see p. XX.)